To inspire and educate our Highmark family so together all can achieve success.

June 2025

Terms and Conditions Update for My Credit Score (by Savvy Money)

We would like to provide further clarification on being enrolled in Credit Score on May 28th. Credit Score is a free service that we are now providing to all members of Highmark Federal Credit Union and using Credit Score will have no impact on your score.

If you decide that you don’t want to use this service, there are three ways that you can turn it off.

- When entering Credit Score for the first time, a tutorial banner will be displayed. On the final page of the tutorial, you will see text that says, “Turn it off or on at any time”. Click on this text and you will be taken to a page that allows you to turn Credit Score off.

- Additionally, you can turn off Credit Score in the Welcome Email that you will receive on the date of enrollment. At the bottom of the email, you will see a button, “Turn off Credit Score”, and by selecting this it will turn it off.

- The final way to turn off Credit Score is within the tool itself. Select the “Resources'' tab on the navigational bar. Then select the “View Now” button under Profile Settings and finally select “Deactivate Credit Score Account'' at the bottom of this page.

You will not be automatically enrolled once you cancel this service. If at any point you would like to re-enroll, the Credit Score widget will be available for you to opt back in.

Thank you and we apologize for any inconvenience.

January 2025

Tax Season Information

Tax forms (Forms 1098 Mortgage Interest and Forms 1099-INT Dividend Income) are being mailed to members this week (1/27/2025). Tax forms will be delivered by US Postal Service to the Primary address on members' accounts. If you don not receive your forms within 10 days and you have moved in the past year, you may need to contact us to update your primary address with us.

Generally, members will receive a Form 1098 from Highmark only if you paid, in aggregate, at least $600 in Mortgage Interest to Highmark during the preceding year. If your mortgage was sold on the secondary market, Highmark does not have access to that financial’ s Form 1098.

Generally, members will only receive a Form 1099-INT if they earned, in aggregate, at least $10 in dividends during the preceding year. However, you will receive a Form 1099-INT if you had any amount in Early Withdrawal Penalties, Interest on a US Savings Bonds, or Federal Income Tax Withholding.

Finally, members can also obtain their tax forms using online banking. Once signed in, click on Documents and select the one titled “tax”.

December 2023

A year-end financial checklist to help you start the new year right

The year is almost over, so now is a good time to conduct a year-end financial checkup. Here are some things to review so that you start the new year on the right foot.

Review Your Budget. Check-in with your budget to make sure it aligns with your saving and spending habits. Are your savings setting you up to hit your short and long-term goals? Were there any big life moments — like having a baby, moving, etc. — that happened that would warrant some likewise big changes to the budget?

Check on Your Investments. Ask yourself the following:

- How are you doing with your investments?

- Are you hitting the employee match on your 401(k)? If not, make it a New Year’s goal.

- What about your IRA contributions?

- Is there any way to max those out?

If you can’t contribute the max, consider increasing them every single year. Also, check in on your stocks and bonds. If you’re not happy with how you’re invested, make a change so that the year ahead is an improvement.

Decide on Debt. The end of the year is a good time to make sure you have a solid strategy for paying down any debts, particularly high-rate ones. Review your loans and credit cards. Are you making inroads or just treading water? If you are struggling to make progress on your debts, consider trying something new, like a balance transfer credit card.

Update Your Goals. Make sure your saving habits are aligned with your long-term goals. If things are off track, make this the year you get going in the right direction.

Do One Thing: Review your budget at the start of every year and after every major life event.

November 2023

a shared blog post from our friends at Savvy Money

How to prevent getting hacked in cyber attacks

How to prevent getting hacked in cyber attacks

Cyber criminals are everywhere and they are constantly on the lookout for a potential scam or hack. That means you need to be just as vigilant. While you can’t prevent software from getting hacked, you can make sure your security is as tight as possible. Here are three tips that can help keep hackers at bay.

Use Authentication

One of the simplest steps you can take to prevent your info from being stolen is to enable two-factor or multi-factor authentication. With two-factor authentication, instead of just using one password to log into a site, you will need a password and one additional verification. Usually, the additional verification is a text or email sent to you with a one-time code.

Get Updated

As we mentioned, you can’t do much to prevent hackers who find security flaws in software. However, there is one thing you can do — keep your software updated. Just as hackers are constantly trying to find weaknesses in software, the teams behind the software are creating patches to fill holes. That means it’s important to update your software as soon as possible because vital security patches are often included.

Get Help

A password manager app is another great way to help keep your info safe from hackers. These apps can not only store your passwords but will generate extremely complicated passwords for you. The organization of a password manager is great. The extra security provided via complex passwords is even better.

Do One Thing: Enable two-factor authentication for sites and apps that use them.

June 2023

More Percentage Yield

What to know about APY

The term “Annual Percentage Yield” (APY) plays an important part in your finances. APY refers to the percentage of interest, you earn on your bank or credit union accounts. Let’s take a look at what you should know about APY.

What is APY?

APY uses compound interest to calculate the return on your interest-earning accounts. Depending on the account, the interest could compound daily, monthly, or annually. Compound interest is the interest added to your principal balance. Let’s say you earn $7 on your $20,000 balance this month. Next month you’ll earn interest on $20,007.

APY vs APR

The terms APY and APR seem similar, but they are different. You can think of it this way: APY refers to the interest you earn, and APR — annual percentage rate — refers to the interest you pay.

APY Variables

Depending on what type of savings account you have, APY can vary. If you have a regular savings account, the APY will fluctuate based on the market. If you have a CD, the rate will stay the same as when you purchased it.

Why APY Matters to You

APY matters because the more money you have saved, the more money you can earn. Compound interest might seem small, but it adds up over time. So when shopping for a savings account, be sure to find the best APY available. Check online banks and credit unions, as they typically offer better APYs for their accounts than big banks.

March 2023

Needs Vs Wants

(Credit to Nerdwallet)

Determining needs

Financial needs are expenditures that are essential for you to be able to live and work. They’re the recurring expenses that are likely to eat up a large chunk of your paycheck — think mortgage payment, rent or car insurance.

Here’s a short list of some common expenses that fall under needs:

· Housing.

· Transportation.

· Insurance.

· Gas and electricity.

· Food.

Identifying wants

Wants are expenses that help you live more comfortably. They’re the things you buy for fun or leisure. You could live without them, but you enjoy your life more when you have them. For instance, food is a need, but daily lunches out are likely more of a want.

Wants typically include things such as:

· Travel.

· Entertainment.

· Designer clothing.

· Gym memberships.

· Coffeehouse drinks.

Wants and needs won’t be the same for everyone.

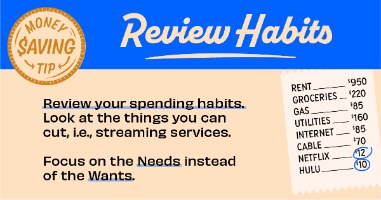

Budgeting for both needs and wants

So how do you start accounting for wants and needs in your budget? Begin by writing a list of all the things you buy. That means everything from toilet paper to life insurance. Then, group purchases into broad categories like toiletries, cable, phone and insurance.

Divide the categories into two buckets: wants and needs. We would place insurance and a basic phone plan under needs, but a Netflix subscription and deluxe cable package will more than likely fall under wants.

Tally the totals and align your priorities. NerdWallet recommends the 50/30/20 budget. If you distribute your monthly income in this fashion, you would spend 50% on needs, 30% on wants and 20% on savings and paying off debt. Plug your monthly take-home income into

this budget calculator to determine how much you have available for each category. Or, consider using Highmark's

My Budget Tracker to better understand where your spending is going.

January 5, 2023

5 Steps To Organizing Your Finances

Do you know your net worth? Or how much you spend each month, and on what? Or how much you can expect from your pension plan or Social Security in retirement? A majority of the population will answer "no," saying they've been too busy with life to get a handle on their finances.

Do you know your net worth? Or how much you spend each month, and on what? Or how much you can expect from your pension plan or Social Security in retirement? A majority of the population will answer "no," saying they've been too busy with life to get a handle on their finances.Fortunately, there's a 5-step action plan to help you take control of your money.

1. Set up a financial filing system either manually or online. Keep separate folders for different expenses and records, for instance "Auto Expenses," "Insurance," "Mortgage," "XYZ Credit Card," etc. There are also many online apps that will allow you to do this electronically. We can help you with that with

My Budget Tracker.

2. Gather records. Look through your records to identify missing information. For example, you need an estimate of your Social Security retirement benefits. To request one, visit SSA.gov or call 800-772-1213. Gather copies of your health, disability, life, homeowners, and vehicle insurance policies, and get a copy of your credit report. You can check your credit report—the summary of your credit activity that generates your credit score—from each of the three major credit reporting agencies once a year for free. Always make your requests from the annualcreditreport.com website, the only site sanctioned by the Federal Trade Commission. Make one request every four months in rotation among the three credit agencies so you can monitor your credit report year-round.

3. Size up your situation. Add the estimated current value of all assets, including your home, car, personal property, savings, investments, and retirement accounts. Next, add all liabilities, including mortgage, credit card balances, and any other outstanding debt. Subtract the liabilities from the assets. This tells you your net worth. Then, make a list of income and expenses by reviewing paycheck stubs, online checking account information or your checkbook register, and credit card statements from the past year. Finally, track spending for a month by saving all receipts or recording cash purchases in a notebook or use one of the many expense tracker or money management apps that can help organize spending by category.

4. Chart a course. Set financial goals—long term and short term—and figure how much money you'll need for each. Create a target saving and spending plan that meets needs using your list of income expenses. For a month or more, track actual spending to see how you're doing, making changes as necessary

5. Brush up on money management basics. Contact or visit us here at Highmark for more help, tips, or information about how to save and spend finances wisely.

December 20, 2022

Steps to take if your identity is stolen

From our friends at Savvy Money

According to a recent study, in 2021, 15 million consumers were victims of identity theft, with criminals using that personal information to create $24 billion in losses. ID theft is a real problem. Here are some steps to take if you should ever become the victim of this crime.

Reach Out

The first thing to do when your identity is stolen is to contact your credit card companies, credit union or bank. If someone is using your Social Security number, you need to contact the IRS. Use this form to navigate the process.

File a Claim

You’ll want to file a claim with the FTC. Head to www.identitytheft.gov and report the incident. As US News reports, not only will filing with the FTC alert them of the scammers, you’ll also receive instructions and forms that can be used to report the thieves to the police and dispute charges to your accounts.

Review Statements

Check your statements and credit report for any fraudulent activity. If anything seems off, report it immediately. And don’t make this a one-and-done. Identity thieves are known for sitting on data until the news of a breach cools down. Keep checking.

Update Your Security

Unfortunately, it’s time to change all of your passwords. Yes, all of them. You can use a password manager app to make this process a little easier.

Freeze Your Credit

You can also freeze your credit with the three major credit bureaus. This way, no one will be able to pull your credit and create fraudulent accounts with your information. To do this, reach out to each bureau individually. It’s free, you can do it online, and you can unfreeze your accounts at any time.

December 8, 2022

Tips On Fraud Prevention

Tip to help you outsmart fraudsters! Fraudsters can make a call, email, or text

look like it’s coming from Highmark Credit Union. Be suspicious of communications asking for sensitive

information. Don’t provide personal information and call us directly at 605-716-4444 or reach out to us via our Contact Page

here

November 25, 2022

What is a money market account?

A money market account is a savings account that may also have debit card and check-writing privileges. The accounts typically limit the number of purchases and transfers to six each month. ATM withdrawals usually are not capped.

Traditionally, money market accounts often offered higher interest rates compared with regular savings accounts. Deposits are insured by the National Credit Union Administration at credit unions. Your money is protected, up to $250,000 per depositor, if the financial institution goes out of business.

What are the pros and cons of money market accounts?

Is a money market account worth it? That depends. If you’re considering one, keep these pros and cons in mind.

Pros

- Better rates than typical checking accounts and some savings accounts.

- Safe place to keep a large chunk of money, protected by FDIC or NCUA insurance.

- Easier access to funds than with traditional savings accounts because of debit card and check features, which might be helpful in an emergency.

Cons

- Some institutions require high minimum balances to open an account or avoid fees.

- Rates are lower compared with some high-yield savings accounts.

- Access to money with checks and debit cards could encourage impulse spending, which might make it harder to save.

See Rates

November 21, 2022

How Many Credit Cards Should I Have?

If you’re trying to build credit or boost your credit score you might be wondering if there is an ideal number of credit cards to have. The truth is there is no perfect number. However, there are factors you should keep in mind when deciding how many credit cards to have.

Your credit score is calculated by looking at five categories, each with varying levels of importance: your payment history (35%), credit utilization (30%), the length of your credit history (15%), new credit (10%), and type of credit used (10%). The first two categories carry the most weight, so focus on getting those percentages as low as possible.

Since payment history makes up 35% of your credit score, make sure you always pay your bills on time. That can be a challenge if you have multiple credit cards with different due dates. To ensure you pay all your bills on time, set alarms or schedule payments so that each one arrives before the due date.

Your credit utilization ratio shows how much of the total available credit you’ve used. To figure out your utilization ratio, first add the balance on all your credit cards. Next add the total amount of credit you have. Then divide your total balance by the total credit. Multiply that by 100 and you have your ratio. To improve your credit score, try to keep that ratio under 30%.

Using multiple cards can also make it harder to keep track of how much you’re spending. Set balance alerts on your cards so you don’t exceed a specified percentage of the card’s available credit.

Rewards cards, which either give you cash back, points for merchandise, or airline miles, generally have higher Annual Percentage Rates (APRs) than other cards, so if you can’t pay the balance on these cards in full every month, it’s best to keep just one or none at all.

September 12, 2022 - What is MFA?

What is it?

Multi-factor Authentication (MFA) is the process of verifying that you are who you claim to be when logging in to a device or an account. If you're reading this from your work computer, you probably logged in to your computer - that's single-factor authentication. But single-factor authentication is no longer enough to keep your accounts secure. Learn more below about the various ways you can digitally authenticate your identity.

Understanding the Types of Identity Claim Factors:

Something you own.

This is using a mobile phone or device that you have in your possession to prove your identity. Typically, the device provides a code via an application, text message, email, or voice call. You then enter this code, and for successful authentication, your code must match what is expected by the service you’re attempting to log in to.

Something you know.

This is something you’ve memorized or stored somewhere, such as a PIN. You must supply the correct PIN to log in to your device or service.

Something you are.

This factor is something about your physical body that cannot be altered, such as your fingerprint or retina. Biometric scanners or readers are used to confirm you’re physically the person that you’re claiming to be.

Why do I need it?

In our digitally-driven world, passwords are no longer enough to keep your information safe. These days, it takes minimal effort for hackers to break into, or social engineer their way into, accounts that are only protected by passwords. Adding an extra step to access your accounts, such as entering an authentication code, means that hackers would also need to have your phone to break in.

Create an additional layer of security and make it harder for criminals to access your data by using two-factor or multi-factor authentication. Consult your IT or Security department to see if your organization has a preferred method of multi-factor authentication.

August 3, 2022 - 10 Ways to Save On Back-To-School Shopping

According to the National Retail Federation, the average American household spends $685 on back-to-school shopping for children in elementary through high school and $943 for young people going to college. Here are 10 ways to save this fall and throughout the year.

1. Create a checklist of items and stick to it.

Before you begin shopping, empty your kids’ backpacks to see what was left over from the previous year. Mark them off your checklist and then buy only the items still remaining.

2. Check to see if your state has a tax-free shopping holiday.

Some states hold tax-free holidays multiple times of the year for particular products. Check out www.taxadmin.org/sales-tax-holidays to see if your state is one of them.

3. Consider shopping without the kids.

They’re more likely to fall for the strategically placed items stores want you to buy. Backpacks and notepads with your kids’ favorite superhero or Disney character can be 30% or more expensive than generic kinds. If your children insist they need an expensive, trendy backpacks, buy stickers and have them decorate their less expensive gear themselves.

4. Comparison shop online before going into stores.

You’ll save on time and gas money.

5. Give your kids a clothing budget and a list of necessities.

You decide what items they must have, then with the remainder of the budgeted money, let them choose what they want.

6. Set up e-mail alerts for sales.

Websites like Dealnews.com, Bensbargains.com, and thekrazycouponlady.com will let you know when coupons or great deals are available for specific items.

7. Buy school supplies in bulk.

Although you’ll have a large initial expense, in the long run the supplies will be cheaper, and you’ll have them on hand for several months.

8. Follow your favorite stores and brands on social media.

You’ll be one of the first to find out when they’re offering deals and special promotions.

9. Go to garage and yard sales (or consignment/used clothing stores) for clothing.

Websites like Garagesalestracker.com, yardsalesearch.com, and Craigslist.org are great online resources for finding bargains in your area.

10. Wait until August or September to buy your school supplies.

That’s when the prices drop significantly. You can even buy for the following year.

June 28, 2022 - Teach Kids Money Management With a Debit Card

Like many parents, you may have opened a savings account for your child when he or she was a baby. If you've been teaching them money management skills and they have shown financial responsibility, then, when they become teenagers, a debit card/checking account from Highmark Credit Union can be a great next step.

As kids hit middle-school age, they start spending more time with friends. That means you're not always around when they buy treats or movie tickets. Those early-teen years can be good opportunities for them to use a debit card and practice financial responsibility.

Though most teens, like most people, no longer write many checks, when the opportunity arises for your teen to write one, jump on it. For example, perhaps your teen pays part of the cell phone bill each month. Have your teen write a check to you for his or her part of the payment. It would be easier just to transfer money from your teen's account to yours but getting practice writing a check once in a while can be beneficial for them.

Explain to your teen the importance of keeping track of the balance in their account either by writing each transaction in a check register or by frequently checking their account online. Also remind your kid that online balances might not show the actual balance in the account if transactions haven't posted or if checks haven't been cashed.

Our team at Highmark is eager to help your teen take this next step financially. Stop by with your teen and we'll show them how to open an account of their own, as well as explain how to use a debit card and our online banking service.

For those of you in the Gillette area, ask about our High School Mascot debit cards - the Camels and the Bolts.

June 21, 2022 - Tap Your Home's Equity

Was your home damaged by the recent hail and heavy windstorms that have been rolling through our area? If so, you might be needing to make repairs or make some changes to your home, and a

home equity loan or home equity line of credit (HELOC) might be your best bet.

These loans let you borrow money using the equity in your home as collateral. Unlike almost any other consumer loan type, the interest on a home equity loan or HELOC of $100,000 or less is likely to be tax-deductible ($50,000 if married filing separately).

With a home equity loan, you borrow a lump sum of money repayable over a fixed term, usually 5 to 15 years, giving you the security of a locked-in rate and a consistent monthly payment. A HELOC is much like a credit card or any other type of open-ended credit. You can borrow money as needed, up to the credit limit your lender assigns, by making a transfer into your checking account. A HELOC is usually a variable-rate loan, so your monthly payments will change based on your outstanding balance and fluctuations in the prime rate.

Talk to the our lenders here at Highmark Credit Union today for more details about our home equity loan products. Stop by or call us at 800.672.6365

June 6, 2022 -

From our friends at Savvy Money, here are some basic tips for savings at the pump:

With gas prices at an all-time high, some ways to save money at the pump

You’ve likely noticed that gas is extremely expensive right now. Your powers of observation are astute: Gas prices are actually at an all-time high. According to the app GasBuddy, the average price of a gallon of gas is now $4.72, the highest it has ever been. Now would be a good time to try and save on gas expenses. Here’s how to do that.

Use an App

Gas tracking apps like GasBuddy and AAA will help you find the cheapest gas near you. This is helpful, because the prices of gas can vary from town-to-town, even street-to-street.

Take Advantage of Clubs

Are you a member of Costco or Sam’s Club? If you are, fill your tank there. These retailers offer members discounted gas and that can save you a ton.

Use Cash

Another way to save money at the pump is to use cash. As USA Today notes, using cash can save you anywhere between 5 and 10 cents per gallon. That might not seem like a lot, but it adds up over time.

Get Rewards

You should sign up for gas station loyalty programs. Pretty much every station has some kind of program. Right now consumers who are members of 7-11’s program get an 11 cents per gallon discount on their first seven fill-ups.

Go Monday

If you can time it right, filling up on Mondays is the way to go. According to reports, Mondays are the cheapest day for gas. Sundays are the runners-up.